Getting out of debt doesn’t have to mean wrestling with complicated spreadsheets or making wild lifestyle changes. A simple debt payoff plan starts with listing all your debts, picking between the snowball method (smallest balance first) or avalanche method (highest interest first), and making extra payments whenever you can.

Most folks who stick with a basic plan can pay off their debt in about 2-5 years. Yep, it really can be that straightforward.

The real challenge? Sticking with your plan when life throws curveballs. Your car breaks down, your income shifts, or you just lose steam after a while.

That’s why successful debt payoff strategies always build in some flexibility and realistic timelines from the start. Otherwise, it’s just too easy to give up.

This guide walks you through creating a debt payoff plan that fits your actual income and expenses. You’ll see how to track your progress, find extra cash for payments, and tweak your plan when things go sideways.

No judgment here about how you got into debt. Just practical steps to help you get out.

- Key Takeaways

- Laying the Groundwork for a Successful Debt Payoff Plan

- Choosing the Best Payoff Strategy

- Executing Your Debt Payoff Plan Effectively

- Maintaining Financial Freedom After Paying Off Debt

- Frequently Asked Questions

- What are the steps to create an effective debt payoff plan?

- How can I use a debt payoff calculator to accelerate my debt reduction?

- Which is better for paying off debts: snowball or avalanche method?

- Can a debt payoff app help me manage and eliminate my debts more efficiently?

- What should I look for in reviews of debt payoff planners?

- How can I pay off a significant amount of debt, such as $30,000, within a set period like 2 years?

Key Takeaways

- Start with a small emergency fund so you don’t go deeper into debt when surprises pop up.

- Pick the snowball method for quick wins or the avalanche method to save more on interest—whichever keeps you motivated.

- Review and adjust your plan every three months as your financial situation changes.

Laying the Groundwork for a Successful Debt Payoff Plan

Getting your debt payoff plan going starts with three things. You need to know exactly what you owe, protect yourself from surprise expenses, and figure out how much you can actually pay toward debt each month.

Assessing Your Debt Situation

You can’t make a debt payoff plan without knowing exactly what you owe. Grab all your statements and jot down every debt.

For each debt, write down:

- Creditor name

- Current balance

- Interest rate (APR)

- Minimum payment amount

- Payment due date

For credit cards, list the current balance—not your credit limit. Don’t guess these numbers. Log in or call your creditors and get the real figures.

Include everything: credit cards, student loans, car loans, medical bills, personal loans, even money owed to family or friends. It’s easy to forget smaller debts or try to ignore the total, but this step shows you the full picture.

Building a Starter Emergency Fund

Before you start throwing extra money at debt, stash a starter emergency fund away. Without that cushion, one car repair or surprise bill can send you right back into debt.

Here’s a rough guide for how much to save:

| Your Situation | Emergency Fund Target |

|---|---|

| Stable job, low expenses | $500-$1,000 |

| Variable income or high expenses | $1,500-$2,500 |

| Self-employed or commission work | One month of expenses |

Keep this money in a separate savings account so you don’t accidentally spend it. Building this fund might delay your debt payoff by a month or two, but it stops you from sliding backward when life happens.

While you’re building this emergency fund, stick to minimum payments on all debts. Once the fund is ready, you can attack your balances harder.

Calculating Your Payoff Power

Your payoff power is just the gap between what you earn and what you spend. That’s what determines how fast you can get debt-free.

Track your real spending for 30 days, or look back over three months of bank statements. Write down your total monthly income after taxes. Subtract every expense, including all minimum debt payments.

The formula: Monthly income – All expenses = Money available for extra debt payments

Most people overestimate this number—sometimes by a lot. Be honest about what you actually spend on groceries, gas, subscriptions, and eating out.

Don’t count on future raises or side hustles that haven’t started yet. If you get irregular bills, like car insurance every six months or annual fees, divide those by 12 and set that aside each month. That way, those bills won’t wreck your plan when they show up.

Choosing the Best Payoff Strategy

There are two main ways to pay off debt: the snowball method and the avalanche method. Each one has its own perks, depending on what motivates you and your financial situation.

Some folks even mix the two to balance savings and momentum.

Debt Snowball Method

With the debt snowball method, you pay off your smallest debt first, no matter the interest rate. Make minimum payments on everything else, and throw every extra dollar at the smallest balance.

Once that’s gone, roll that payment into the next smallest debt. The process builds momentum as you knock out balances one by one.

Key benefits:

- Quick wins that keep you going

- A sense of accomplishment as accounts close

- Easy to follow

- Great if you need encouragement to stick with it

The snowball method works best for people who need to see progress to stay motivated. Watching a credit card hit zero in a few months can fire you up way more than slow interest savings. Studies show people with written debt payoff plans are 42% more likely to succeed, and the snowball approach helps a lot of folks stick with it.

Debt Avalanche Method

The avalanche method goes after your highest interest rate debt first, while you pay minimums on the rest. Once that’s gone, you move to the next highest rate.

This strategy saves you the most money over time. High interest rates make debts balloon, so tackling those first cuts your total interest payments.

Key benefits:

- Saves the most on interest

- Gets you out of debt faster (on paper, anyway)

- Makes the most of your money

- Logical, numbers-driven approach

The avalanche method is best for people who care more about long-term savings than quick wins. If you’ve got a big chunk of high-interest credit card debt, avalanche can save you a lot more than snowball. But it might take longer to wipe out your first debt, which can feel discouraging.

Hybrid Payoff Approaches

You don’t have to pick just one method. Many people blend strategies to get the best of both worlds.

One popular hybrid is to start with the snowball method to knock out a couple of small debts fast. Those wins build confidence and free up some cash flow. Then, switch to the avalanche method for the high-interest stuff.

Or, you can rank debts by both balance and interest rate. Maybe you target a medium-sized debt with a high rate first—so you get a win and save money.

Hybrid strategy perks:

- Mixes motivation and savings

- Lets you adapt as life changes

- Gives some breathing room if you hit a setback

- Balances emotion and logic

The best payoff strategy is the one you’ll actually stick with. Think about your personality and habits. If you need to see results to keep going, start with snowball. If you love numbers and logic, go avalanche. Your situation decides what works best.

Executing Your Debt Payoff Plan Effectively

Paying off debt takes more than just good intentions. You need a clear schedule for when each debt will be gone, a way to track your wins, and enough flexibility to handle surprises without giving up.

Creating a Realistic Payoff Schedule

Your payoff schedule lays out every payment from today to your debt-free date. List all your debts with current balances, interest rates, and minimum payments.

Decide how much extra you can pay each month beyond the minimums. Use that number to estimate your payoff timeline for each debt.

If you’re using snowball, hit the smallest debt first. With avalanche, focus on the highest interest rate.

Write down the month and year each debt will be paid off. Having real milestones beats vague goals like “pay off debt soon.”

Add a buffer—maybe 10-15% more time than you think you’ll need. So, if you plan on 24 months to pay off debt fast, expect it might take 27. Life happens, and you’ll thank yourself for not being too optimistic.

Tracking Progress and Staying Motivated

Track progress every month by writing down each debt balance on a set date. Some people pick the first of the month, others use payday.

Keep these numbers in a spreadsheet, notebook, or even an app. Add up your total debt every month and watch it shrink. Seeing $15,000 drop to $14,200 proves your plan is working, even if each payment feels small.

Set up visual reminders—a chart on your wall, or a phone background with your debt-free date. Color in sections as you go. These little cues help keep your goal front and center, especially when you’re tempted to spend.

Celebrate your wins, but don’t blow money doing it. When you finish off a debt, tell a friend or share it online. That recognition keeps your motivation alive for the next round.

Adjusting to Life Changes

Your income and expenses will shift during your payoff journey. Review your plan every three months to adjust for changes.

If you get a raise, try to redirect at least half the increase to debt payments. If expenses go up, temporarily reduce your extra payment instead of stopping it altogether.

When unexpected costs hit, dip into your emergency fund first. Rebuild it before you go back to aggressive debt payments.

This way, you avoid piling up new debt while you’re trying to become debt-free. It really does help in the long run.

If you lose your job or your income drops, change your plan right away. Switch to minimum payments only until things stabilize.

Once your income comes back, restart extra payments at whatever level you can handle. Pausing is way better than giving up.

Big life changes like marriage, divorce, or moving always shake up your finances. Recalculate your payoff timeline with your new numbers.

The method itself doesn’t change, even if the details do. Just keep tweaking as life happens.

Maintaining Financial Freedom After Paying Off Debt

Once you wipe out your debt, it’s important to protect that progress. The money you used to send to creditors can finally work for your future.

Budgeting for a Debt-Free Life

Your budget needs to shift now that debt payments are gone. Take the amount you were paying toward debt each month and split it into three categories: savings, investments, and lifestyle improvements.

Start by directing at least 50% of your former debt payment into savings. This helps you build your emergency fund from the starter amount to a full 3-6 months of expenses.

A strong emergency fund helps maintain financial stability after becoming debt-free.

Monthly Budget Adjustments:

- Emergency fund: 30-40% of old debt payment

- Retirement savings: 20-30% of old debt payment

- Short-term goals: 20-30% of old debt payment

- Lifestyle improvements: 10-20% of old debt payment

Track your spending every month to spot budget creep. It’s easy to let spending rise once debt disappears, but that can eat away your hard-won progress.

Avoiding Common Debt Pitfalls

Try not to slip back into the spending patterns that caused debt in the first place. The freedom you feel after paying off debt can tempt you to reward yourself, but that can backfire.

Set clear rules about credit card use. Pay your full balance every month or just stop using cards for a while.

Many people who pay off debt find that keeping their debt payoff routine helps them stay accountable after reaching their goal.

Watch out for lifestyle inflation when you get raises or bonuses. Instead of upgrading everything, increase your spending by only 20-30% of any income boost.

Put the rest toward savings and investments. Create spending alerts on your accounts so you catch unusual patterns early.

Review your budget every quarter to adjust for life changes, but keep your core financial habits steady.

Frequently Asked Questions

Getting out of debt raises a ton of practical questions. People want to know which methods actually work and how to stay on track. The answers below tackle common concerns about plans, tools, and those big, intimidating balances.

What are the steps to create an effective debt payoff plan?

Start by listing all your debts with their balances, interest rates, and minimum payments. Write down each creditor, how much you owe, and when payments are due.

Subtract all your necessary expenses from your monthly income. That shows you how much extra you can send to debt each month.

Build a small emergency fund of $500 to $1,000 before throwing extra at debts. This keeps you from falling back into debt when life throws surprises.

Choose either the snowball method (smallest debts first) or avalanche method (highest interest first). Pick the one that fits your personality and keeps you motivated.

Set up automatic payments for at least the minimum on every debt. Then put all extra money toward your chosen target debt until it’s gone.

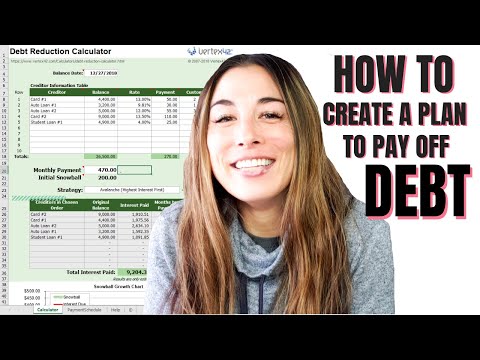

How can I use a debt payoff calculator to accelerate my debt reduction?

A debt optimizer calculator takes your interest rates, balances, and minimum payments to build a personalized strategy. Enter your info to see exactly when you’ll be debt-free.

The calculator shows how much interest you’ll save by paying extra each month. Even an extra $50 or $100 can shave years off your timeline.

Use the calculator to compare different payment scenarios. Try out what happens if you earn extra income, cut expenses, or switch up your payment strategy.

Update your numbers in the calculator every few months as your balances drop. Watching your debt-free date move up feels pretty great.

Which is better for paying off debts: snowball or avalanche method?

The snowball method knocks out your smallest debts first, no matter the interest rate. You make minimum payments on everything else and put all extra money toward the smallest balance.

The avalanche method goes after your highest interest rate debt first. Over time, this saves you the most in interest charges.

Pick snowball if you need quick wins to stay motivated, especially if you have several small debts under $1,000. Paying off an entire debt in just a few months can build serious momentum.

Go with avalanche if you’re focused on long-term savings and your biggest debts have the highest rates. It’s a little less exciting at first, but you save more in the end.

If your debts’ interest rates are all pretty close, the boost from snowball usually beats the minor savings from avalanche. Some people use a hybrid approach—clear one small debt for motivation, then switch to the highest interest rates.

Can a debt payoff app help me manage and eliminate my debts more efficiently?

Debt payoff apps let you see all your balances in one spot. No need to log into a dozen different accounts.

They send reminders before payments are due so you avoid late fees. Many apps show charts or progress bars that update as you chip away at your debt.

Seeing your total debt number drop each month is motivating. Some apps even suggest which debt to target next based on your chosen method.

They calculate your debt-free date and show how extra payments change your timeline. Look for apps that sync with your bank accounts so updates happen automatically.

Manual entry is a pain and can lead to mistakes. Free apps usually cover basics like tracking and reminders, while paid versions may offer custom payoff plans or spending analysis.

What should I look for in reviews of debt payoff planners?

Read if reviewers mention ease of use and a clear interface. Overly complex tools with tons of features often get ditched after a few weeks.

See what people say about calculation accuracy and realistic timelines. You want a planner that matches your actual payment amounts.

Check what users report about customer support if you’re considering a paid planner. Good help matters when you hit a snag.

Notice if reviews mention staying motivated. Features like progress tracking and celebrating milestones can make a difference.

Look out for complaints about hidden fees or surprise charges with paid services. The cost should match the value you get.

How can I pay off a significant amount of debt, such as $30,000, within a set period like 2 years?

Paying off $30,000 in two years means you’ll need to come up with about $1,250 each month, plus interest. All in, you’re probably looking at monthly payments closer to $1,400, so your income has to stretch far enough after the basics.

To close that gap, you might want to boost your income with side gigs, overtime, or even a second job. Plenty of folks pick up freelancing or part-time work for 10-20 hours a week just to tackle debt faster.

Cutting expenses is huge. Maybe you downsize your living situation, sell a car, or cut out most extras. Honestly, moving to a smaller place or finding a roommate could free up anywhere from $300 to $800 each month, which feels like a game-changer.

Whenever you get a windfall—like a tax refund, bonus, or random gift money—just throw it straight at your debt. For example, a $3,000 tax refund knocks out 10% of your goal in one shot.

Using the avalanche method to minimize interest charges can really help when you’re dealing with big balances. Tackling high-interest debt first saves a surprising amount over two years.

If your credit’s good, you might try a balance transfer to a 0% APR card and pay it off during the promo period. That’s one way to dodge interest entirely, but you’ve got to stay disciplined and not rack up more debt.